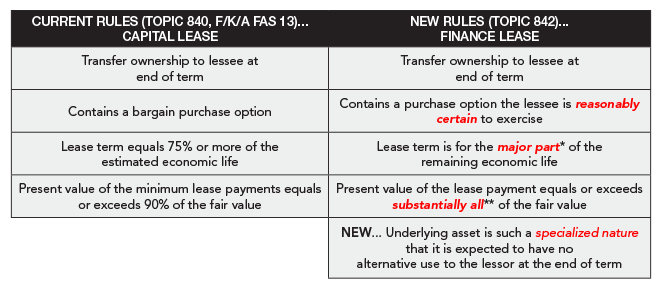

In February 2016, the Financial Accounting Standards Board (the “FASB”) issued a new lease accounting standard (Topic 842). The new lease accounting standard will impact financial reporting for entities that are required to report their financial results in accordance with U.S. generally accepted accounting principles. Topic 842 does not impact the tax treatment of leases. In addition, Topic 842 will not impact the many economic benefits realized by utilizing leasing as a source of financing. Leasing is still a great way to offer products to your customers and will continue to be an attractive financing option for your customers!

What are the effective dates for the FASB changes?

Topic 842 was effective for public companies for fiscal years beginning after December 15, 2018, and is effective for private companies for fiscal years beginning after December 15, 2021. Early adoption is permitted for all entities. Upon adoption, companies will be required to recognize and measure leases at the beginning of the earliest period presented in their financial statements or, alternatively, companies can recognize and measure leases at the adoption date along with a cumulative-effective adjustment to retained earnings. Although the new standard will be applied to all active leases at the time of transition, lessees may not be required to reassess lease classification upon transition.

NOTE: our experts have produced additional resources for you and your team, view them now.

Many entities have begun the process of evaluating the potential impacts of the new lease accounting standard. In addition to consulting with lenders, lessees should also consider consulting with their auditors regarding how the new standard will impact their financial statements, and their technology and software providers regarding changes to support the new standard.

Further resources:

Download a two-page flyer outlining the details about the FASB Topic 842 changes to share with your team.